Artificial intelligence (AI) can help significantly increase output for office workers.

Breakthroughs in artificial intelligence (AI) are advancing so quickly, it’s getting harder to imagine a world in which the technology isn’t impacting just about every facet of daily life.

While much of the chatter surrounding AI has revolved around areas such as accelerated computing and healthcare, there’s another use case that’s piqued my interest. Integrating artificial intelligence into the corporate workforce represents a unique and compelling long-term opportunity.

Ark Invest CEO Cathie Wood has declared that AI software has the ability to significantly increase productivity in the workplace. In a recent report, Wood suggests that AI automation software could be a $13 trillion market in 2030.

Believe it or not, there are a host of companies focusing on building more efficient workplace environments through the power of technology. UiPath (PATH -1.52%) is a leading player in AI-powered automation tools, and I think it could be the best investment option in this pocket of the AI realm.

Let’s break down how AI can redefine workplace dynamics and assess why UiPath is a compelling long-term opportunity.

Workplace productivity is ripe for disruption

Bringing efficiencies to basic tasks is not a new idea. In many cases, technology has been the key to unlocking these gains.

In Ark Invest’s Big Ideas 2024 report, Wood presents some interesting case studies related to robotics and how they’ve enhanced completing mundane and administrative aspects of labor.

For example, Wood says that the advent of the washing machine cut down the average time to do laundry by 87%. Similarly, integrating assembly lines into factories significantly reduced the time needed to manufacture a car.

These ideas have been applied to the workplace for decades. For example, sales and marketing leaders have relied on customer relationship management (CRM) tools from the likes of Salesforce for many years.

Moreover, enterprise resource planning (ERP) suites from SAP and Oracle have facilitated some of the largest businesses in the world when it comes to aggregating financials, analyzing operating metrics, and more.

According to Wood, by automating tasks through artificial intelligence, the average worker’s productivity could increase by 4.5x. If all of the potential software vendors captured just 10% of the productivity gain, Wood posits, these companies could reap $13 trillion in combined revenue.

This scenario implies that UiPath has a greenfield opportunity as it relates to the intersection of AI and workplace productivity. Let’s dive into how the company is actually performing, and how it stacks up against the competition.

Image source: Getty Images.

UiPath is leading the charge

UiPath operates in the robotic processing automation (RPA) market. Essentially, the company’s software helps automate administrative tasks and boost workflow processes.

UiPath ended last year with over 2,000 customers spending at least $100,000 per year on its platform. Moreover, UiPath increased its customer count by 26% year over year for those spending at least $1 million per year on its software suite. This highlights UiPath’s deep penetration in both small and midsize enterprises (SMEs) as well as larger corporate accounts.

The accelerated customer adoption isn’t entirely surprising given how much demand for AI has risen over the last year. The company increased revenue by 24% last year to $1.3 billion. Meanwhile, adjusted free cash flow was $309 million. By comparison, the company was essentially breakeven on a free-cash-flow basis during the prior year.

With an impressive partner ecosystem that includes SAP, IBM, Accenture, PwC, and Deloitte, I think UiPath’s growth story is just getting started.

A compelling valuation narrative

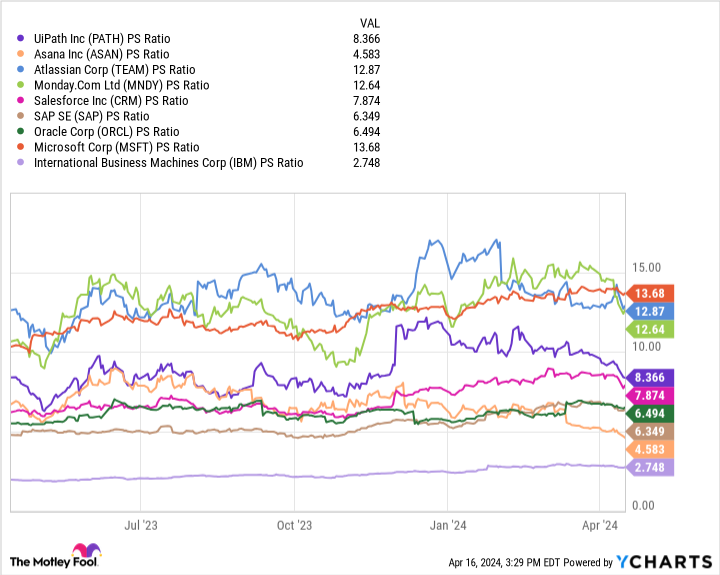

The chart below benchmarks UiPath against a cohort of other enterprise software platforms that offer workplace productivity solutions. With a price-to-sales (P/S) ratio of 8.4, investors can see that UiPath is positioned right in the middle of this peer set.

PATH PS Ratio data by YCharts

What I find most interesting about the analysis above is that UiPath is valued more in line with the larger tech behemoths operating in the RPA space — with Microsoft being the lone exception. Given the success Microsoft has demonstrated through its CoPilot platform, it’s not entirely surprising to see it trading at such a noticeable premium among this peer set.

Keep in mind that UiPath ended last year with about $2 billion of cash and equivalents on its balance sheet. Although the company is cash-flow-positive, one item to consider is how the company will allocate its resources. In order to compete with big tech behemoths at scale, UiPath will likely need to increase spending.

While that would impact the company’s bottom line, it could be a worthwhile strategy. I’m optimistic about the efficiencies that AI can bring to the workplace in the long run, and am aligned with Wood’s theory that the market opportunity is enormous.

So far, UiPath has proven that it can compete in the RPA market against larger and better-capitalized enterprises. Given how fast AI is impacting other important end markets, I think it’ll be sooner rather than later that the technology will begin to make serious impacts on workplace environments.

I think now is a good time to consider scooping up shares in UiPath as productivity becomes more of a focal point for businesses of all sizes.

Adam Spatacco has positions in Microsoft. The Motley Fool has positions in and recommends Accenture Plc, Asana, Atlassian, Microsoft, Monday.com, Oracle, Salesforce, and UiPath. The Motley Fool recommends International Business Machines and recommends the following options: long January 2025 $290 calls on Accenture Plc, long January 2026 $395 calls on Microsoft, short January 2025 $310 calls on Accenture Plc, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

{kind=link}